House prices across all English Cities have risen above pre-crisis peaks for the first time since 2007, according to the latest Zoopla UK Cities House Price Index – the index from the UK’s most comprehensive property portal.

The overall annual rate of house price growth across all UK cities is close to a three-year high (33 months), with price growth pegging level at 3.9 per cent from December 2019 to January 2020.

A pick-up in the headline rate of growth was bolstered by increased growth across southern cities, following a period of broadly flat price performance over 2019.

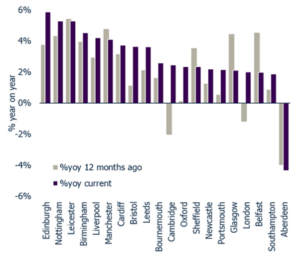

All cities, except for Aberdeen (which stands at -4.3 per cent), are recording annual house price inflation of at least 2 per cent per annum, for the first time since February 2017. City growth is led by highs of +5.9 per cent in Edinburgh, and +5.3 per cent in Nottingham and Leicester.

Figure 1: City house price inflation – current compared to 12 months ago

Source: Zoopla UK City House Price Index, powered by Hometrack

Regional variation in recovery

City-level markets have seen prices develop at different speeds across the housing cycle.

Central London was the first market where prices surpassed 2007 levels, with average values reaching their pre-crisis peak in two and a half years. Prices were buoyed by overseas buyers entering the market, attracted by a major drop in the value of sterling, which made dollar-pegged purchases look like even better value.

London’s return to form was closely followed by southern cities, which returned to pre-crisis levels within seven years, boosted by rising demand and employment growth.

Meanwhile, Newcastle was the final English city in Zoopla’s UK Cities index to reach this milestone, some 12 years after the financial crisis. Average values in the city surpassed the levels last seen in 2007 in late December 2019. While the north east as a region has lagged behind the rest of the country in terms of house price recovery, Newcastle’s house prices fell the furthest in the aftermath of the financial crisis and had the furthest distance to recover.

Demand outstrips supply

Zoopla data shows how demand is outstripping supply*, helping to exert upward pressure on prices in some markets. On the supply side, the stock of homes for sale rose by an average of 2.6 per cent year on year in January 2020. This contrasts with the strong bounce in demand, which was up by 26 per cent over the same period, according to Zoopla data. This is reflected in data for mortgage approvals**, which shows demand up 5 per cent in December 2019, compared to a year earlier.

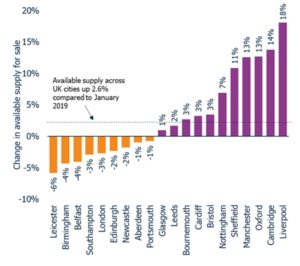

Despite the apparent upsurge in supply at a national level, stock levels in nine cities are tracking lower than a year ago by as much as 6 per cent.

Of the three cities registering annual price growth of more than 5 per cent, Edinburgh (5.9 per cent) and Leicester (5.3 per cent) have fewer homes available for sale than a year ago, with stock in Edinburgh down 2 per cent, and Leicester down 6 per cent.

Figure 2: Stock of homes for sale in January 2020 compared to January 2019

Source: Zoopla UK City House Price Index, powered by Hometrack

Commenting on the latest report, Richard Donnell, Research and Insight Director at Zoopla, says: “It has taken twelve years for house prices in all English cities to return to their previous pre-crisis levels. Some cities returned to 2007 levels within four years, as the economy and job growth rebounded. In others, it has taken much longer as the mismatch between demand and supply has been less pronounced.

“An imbalance between supply and demand is supporting the current rate of house price growth – a trend we expect to remain in place over 2020H1. Strong demand and attractive affordability are sustaining above average price growth in Nottingham despite an increase in supply. The same will apply to other cities including Liverpool and Manchester. The growth in supply in Oxford and Cambridge is more likely a result of sellers, who were sitting on their hands waiting for market conditions to improve, before eventually deciding to make their move, encouraged by improving housing market sentiment.

“We do not expect a material acceleration in the rate of growth in the foreseeable future, as affordability pressures will limit the scale of price growth, especially across southern England.

“There is a risk that, in some markets, sellers may become unrealistic about the expected sales price for their home. This is more likely in London and southern England where the market has been weak, and supply remains constrained. Housing demand is up, but there remains a price sensitivity amongst buyers, especially in the highest value markets.

“The upcoming Budget is a prime opportunity for the new Chancellor to address some of the factors affecting the housing market. Any review of stamp duty charges to help the movement of homeowners up and down the property ladder should be made to boost transaction levels, but the extent and nature of any reform, which must be balanced against political exigencies, remains to be seen.”

*Supply: Change in supply compares total number of active sales listings in month of Jan 2020 compared to Jan 2019

**Bank of England